UPDATE: Tokyo’s core consumer prices eased to 2.3% in December 2023, falling short of market expectations of 2.5%, but remain above the Bank of Japan’s (BOJ) target of 2%. This significant development indicates that while inflation is cooling, it has not collapsed, keeping the central bank’s policy normalization on track.

Authorities report that the rise in consumer prices, excluding fresh food, slowed from 2.8% in November. The deceleration is largely attributed to lower utility and energy costs, combined with a moderation in food price increases. The “core-core” inflation measure, which excludes both fresh food and energy, also softened to 2.6% year-on-year from 2.8%, while the headline CPI dropped to 2.0% from 2.7%.

This shift marks the first clear easing in Tokyo’s inflation momentum since August, reinforcing the notion that underlying price pressures remain persistent. The Tokyo CPI is widely viewed as a key indicator for national trends, suggesting that inflation is on a gradual decline rather than facing a steep downturn.

Following last week’s announcement, the BOJ increased its policy rate to 0.75%, the highest level in nearly three decades. BOJ Governor Kazuo Ueda emphasized that further tightening is expected if wage and price trends align with the central bank’s outlook, but refrained from providing specific guidance on the pace or terminal levels of future increases.

Market analysts interpret the December CPI data as consistent with the BOJ’s baseline scenario: inflation is easing as energy effects diminish, yet remains robust enough to warrant ongoing rate hikes over time. Expectations are for a gradual increase in rates approximately every six months, targeting a terminal level near 1.25%, contingent upon continued solid wage growth.

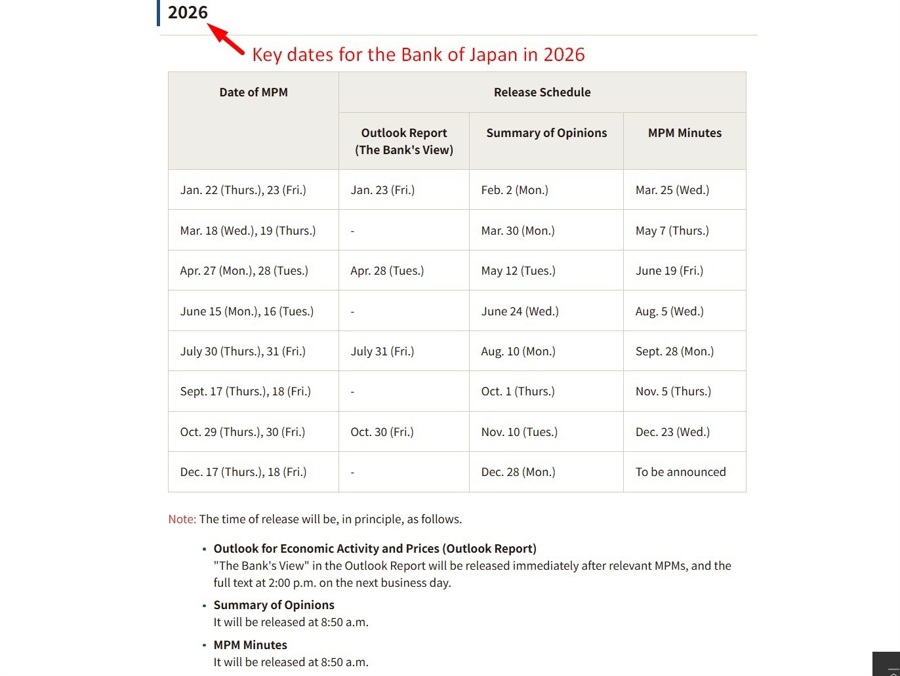

The softer-than-anticipated core inflation print slightly alleviates pressure for an immediate rate hike but does not significantly alter the overall tightening trajectory. With core inflation still exceeding the target and supportive wage dynamics, the BOJ is expected to proceed cautiously. A pause in rate hikes is likely at the next scheduled meeting on January 22–23, 2026.

Market reactions are already evident, with fluctuations in the Japanese yen, JGBs (Japanese government bonds), and the Nikkei. Investors are closely monitoring these developments for insights into future monetary policy and economic conditions.

This latest data underscores the complex landscape facing the BOJ as it balances inflation control with economic growth. The impact of these decisions extends beyond Japan, influencing global markets and economic sentiments.

Stay tuned for further updates as this story develops.